In Wednesday’s post I gave you Part 1 of my thoughts on the GOP’s newly unveiled bill to “repeal & replace” Obamacare. Here’s the continuation of that post . . .

8. The GOP bill essentially defunds Planned Parenthood by forbidding them from getting Medicaid reimbursements. Of the federal funding Planned Parenthood receives, about 75% comes through Medicaid reimbursements (the rest is through Title X grants). Federal law already prohibits any federal funds from being used for abortions. It’s called the Hyde Amendment. And in the case of Planned Parenthood, the funds are not fungible, because the government only reimburses Planned Parenthood after the fact, for specific services rendered. It’s not like a lump sum grant where the money can be moved around to wherever they want to use it. So this is just a nonsense provision to pander to the religious right.

News came out a few days ago that President Trump had made an offer to Planned Parenthood that it could keep its funding if it would stop performing abortions. They of course turned him down.

Also, the new GOP plan prohibits people from using the plan’s tax credits toward any insurance plans that cover abortion. This will likely mean that ultimately, no insurance plans will end up covering abortion, as fewer and fewer people buy such plans. So eventually even those who want and can afford to purchase them without tax credits won’t have the option.

9. As I mentioned in Part 1 of this post, the GOP plan retains Obamacare’s protections for people with preexisting conditions. However it sort of becomes “protection in name only” because the way the GOP plan works will make insurance unobtainable for many of these people. The bill repeals the individual mandate (technically just the mandate’s penalties, but effectively that gets rid of the mandate).  Instead the bill says that anyone who does not maintain continuous coverage of health insurance (meaning they go without for more than 2 months) will have to pay 30% extra in premiums for one year when they do decide to get insurance again.

Instead the bill says that anyone who does not maintain continuous coverage of health insurance (meaning they go without for more than 2 months) will have to pay 30% extra in premiums for one year when they do decide to get insurance again.

This is bad for two reasons. It will do almost nothing to push healthy people to get insurance. Even with the individual mandate, one of the weaknesses of Obamacare is that not enough young & healthy people are signing up. The GOP’s continuous coverage provision is a much, much weaker nudge to get young & healthies into the market. And you need them in the insurance market to balance out the risk pool, as a balanced risk pool is the key to making insurance work.

But there’s a worse problem here: let’s say one of those young & healthies has been without insurance for a few months or years, and then they get a raise at work or they just have an epiphany and decide it’s not sensible to go without insurance. Now if they want to sign up, it’s going to be even more expensive for them with that 30% penalty. So they’re actually discouraged them from going ahead and entering the market at that point.

So who will sign up for insurance at those higher rates?  Mostly just the people who really need to. Of course there will still be some healthy people signing up. Plenty of healthy people don’t want to risk walking around without insurance, and if they can afford it, they’re going to get it. But for people who have to budget their expenses, the only ones who are going to be willing to sign up when they have to pay a penalty for doing so, those are going to be the people who need to sign up, in other words, people who have become sick or injured and now need the insurance.

Mostly just the people who really need to. Of course there will still be some healthy people signing up. Plenty of healthy people don’t want to risk walking around without insurance, and if they can afford it, they’re going to get it. But for people who have to budget their expenses, the only ones who are going to be willing to sign up when they have to pay a penalty for doing so, those are going to be the people who need to sign up, in other words, people who have become sick or injured and now need the insurance.

This could ultimately end in the exact thing that Republicans have falsely claimed for years was happening to Obamacare: the dreaded death spiral. And even if it doesn’t become that dire, it will certainly cause insurance premiums to spike. And for many people who really need insurance, it will become out of reach.

Oh, and PS, that 30% surcharge – it goes to the insurance companies as extra profit. The Obamacare penalty was paid as a tax to the government and then used to help pay for . . . Obamacare, making it possible to fund insurance for more people.

10. So now seems like a good time to mention that Republicans have no idea how they’re going to pay for their plan. The bill repeals all of the Obamacare taxes (taxes that were almost entirely paid by the wealthy, a fact which some people think almost entirely explains Republicans extreme antipathy for the law), except for one, the “Cadillac tax” on very expensive employer-sponsored plans. And that tax is delayed till 2025, so ultimately it will probably be repealed too. They expect to pay for some of the bill with the savings they’re getting from their big Medicaid cuts, but that won’t cover all of it. Lucky for us, the House GOP prepared an FAQ on their website, and one of the questions addressed this:

How are you paying for this plan? How much is it going to cost taxpayers?

We are still discussing details, but we are committed to repealing Obamacare and replacing it with fiscally responsible policies that restore the free market and protect taxpayers.

Good to know they’ve got that covered.

11. The tax credits in the GOP plan are flat credits that (mostly) vary only by age range, as opposed to the Obamacare subsidies, which vary by recipient’s income and by the cost of plans where they live, so that lower income Americans are never paying more than a specified percentage of their income no matter how expensive plans are in their location. Under the GOP plan, all 30 year olds will receive the same tax credit, no matter their income, no matter how much insurance costs where they live.  The only income variation in the GOP plan is that the credits begin to phase out once a person starts making $75,000 and eventually fade to zero (a prior version of the plan gave everyone the credits no matter how high their income).

The only income variation in the GOP plan is that the credits begin to phase out once a person starts making $75,000 and eventually fade to zero (a prior version of the plan gave everyone the credits no matter how high their income).

Because the credits are done this way, the GOP plan disproportionately hurts people who are low income, older or who live in rural areas (where fewer choices tend to mean higher premiums), when compared to Obamacare. It hurts the low income, of course, because their income will no longer be taken into account in determining the amount of the credit. So under the new plan they will receive much less assistance than they’re receiving under Obamacare (also, certain of these people who would’ve been able to get Medicaid under Obamacare will no longer be able to).

It hurts the older and the rural customers because their insurance options are much more expensive than other people’s, but the amount of their credit won’t vary to take this into account (older people get a larger credit than younger people, but not nearly large enough to make up for how much more they pay in premiums).

Additionally, under the GOP plan, the government will be spending a fair amount of tax credit money on (relatively) higher income people that they’re not currently spending under Obamacare.

Adding to the harm for older Americans, the GOP plan will allow insurance companies to charge older customers even more than they can under Obamacare. Obamacare allows companies to charge older customers 3 times as much as younger customers. Under the GOP plan that ratio will be 5 to 1. So while the financial assistance will be getting worse for older people, their plans will be getting more expensive relative to everyone else. Interestingly older and rural voters were much more likely to have voted for Donald Trump. And now they are among the group that will be most hurt by this new plan.

Sick people will of course also be hurt by the new tax credit system, because as explained in #8 above, insurance premiums are likely to become more and more expensive as healthier people drop out of the market. Sick people won’t be able to forgo insurance, and as these tax credits are much less generous than the Obamacare subsidies and also do not adjust for the person’s income or the price of the local market, the financial assistance will buy them less and less over time.

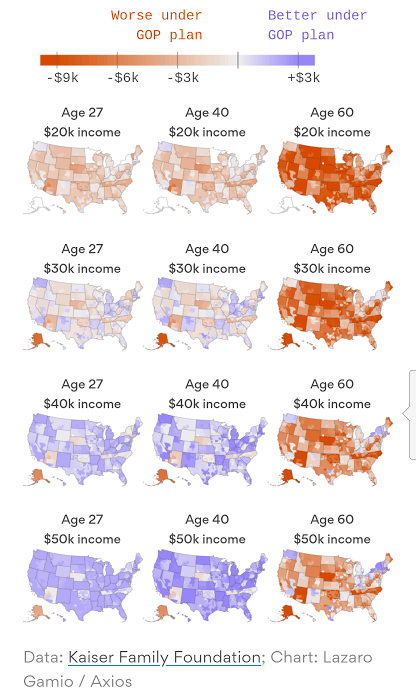

Using data compiled by the Kaiser Family Foundation, Axios put together these maps that compare the difference in tax credits under Obamacare vs the GOP plan in different locations around the country, in 2020 (the year it takes effect). These maps make it easy to see that those who are younger and those who are (relatively) better off income-wise benefit much more under the GOP plan:

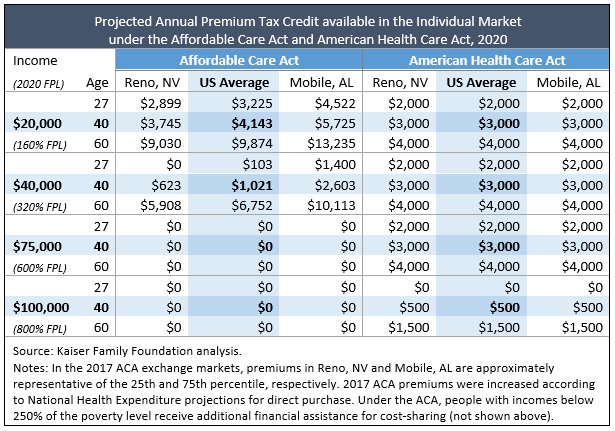

This chart using Kaiser data is helpful in showing why it’s important that Obamacare’s subsidies vary with the cost of premiums around the country. Here’s how Obamacare (Affordable Care Act) and the GOP plan (American Health Care Act) would work differently in two different cities: Reno, NV where premiums are on the low end of the range, and Mobile, AL where they’re on the high end:

12. A lot of people are saying – I would never say it of course, but a lot of people are saying – that between the big tax cuts for the wealthy and the major cuts in funding for poor and lower income Americans, the GOP bill is like the worst caricature of the Republican Party made real.

13. The GOP keeps trying to sell this plan by telling us it will bring prices down and give us more choices of plans and doctors, but they haven’t told us anything about how that’s supposed to happen. I don’t see anything in the new plan that would make either of those things more likely to happen than under Obamacare, and so far if anything, out-of-pocket expenses for most people seem likely to increase.

I don’t see anything in the new plan that would make either of those things more likely to happen than under Obamacare, and so far if anything, out-of-pocket expenses for most people seem likely to increase.

A group of health care experts did the calculations for Vox and found that the average current Obamacare customer would pay $1542 more per year if the GOP plan were to begin today ($2,409 in 2020 when the new plan is actually set to begin). The increase would be most severe for those in the 55-64 age range, with a cost increase of $5269 today ($6,971 in 2020).

Another study out this week found that the GOP plan would lead to premium increases of 30% or more in 2018 and even greater increases in the years after that.

If the “essential health benefits” requirement is removed later as I mentioned in Part 1 that Trump and Tom Price seem to hope to do administratively (though it’s unclear if they’ll be able to do so) that could allow for cheaper plans, but also plans that in many cases will be pretty worthless. Also, the change in the age ratio mentioned in #11 above (allowing insurance companies to charge older customers 5 times as much as younger customers) will probably lower premiums for the youngest age groups. (But it will also raise them for the oldest).

14. And possibly the most ridiculous moment of this entire ridiculous process: Republicans are still obsessing about page numbers. When Obamacare first passed, Republicans just couldn’t get over how long the bill was. It was just too. many. pages. for them. The length of the bill, in their minds, was prima facie evidence of its evilness. In any discussion/argument over the merits of Obamcare, they would just whip out the page count and drop the mic, argument over. Over the years, that’s faded out to a large degree, but it never entirely went away. Tuesday, at a combo Sean Spicer/Tom Price press conference to talk about the new bill, the page number obsession made a comeback in a big way, props and everything.

On the stage with them, they had a table with two stacks of paper – one tall one, and one very short one. As Price spoke about the virtues of the GOP bill, he pointed to the smaller stack of paper (the GOP one) and used that as evidence that the GOP bill was better. But the action really got going when it was Spicer’s turn to speak. He brought out the full Melissa McCarthy effect to discuss the size comparison between Obamacare and the new GOP bill. He must have made the comparison in 4 or 5 different, very excited ways before moving on to other, more substantive topics. Then, after a few minutes, he came back again to the difference in page numbers in the bills, leaning over to the table and pointing, to make sure everyone could see how much smaller the GOP stack was than the Obamacare stack.

(By the way, this argument is especially asinine here because the GOP’s entire “repeal and replace” bill is built off of the text of Obamacare. The ultra-conservatives grumbling about this plan have a point – Obamacare isn’t technically being repealed. It stays intact as the foundation for the new bill, and then the GOP bill just goes into it and repeals or amends specific sections or lines. So you could actually say that the GOP bill is even longer than Obamacare, because it’s the original text of Obamacare, plus all of their revisions. But that would be petty . . .)

Anyway, this display was really the perfect distillation of what the GOP has become – on healthcare especially, but really on most every topic. There is almost a complete absence of substance or depth or any serious thinking. It is all about slogans and sound bites, marketing and whatever clever shows they can put on to rile up their base. In Trump, they have found their perfect frontman.

3 thoughts on “You Down With GOP? (Part 2)”